Juspay HyperUPI - Plugin SDK powering In-App UPI Payments

HyperUPI - In-App UPI Payments.

We are announcing the launch of HyperUPI - your In-App UPI Payments with JUSPAY UPI Plug-in SDK. Improve Conversions and power seamless customer experiences with native UPI Payments in your app.

Introduction

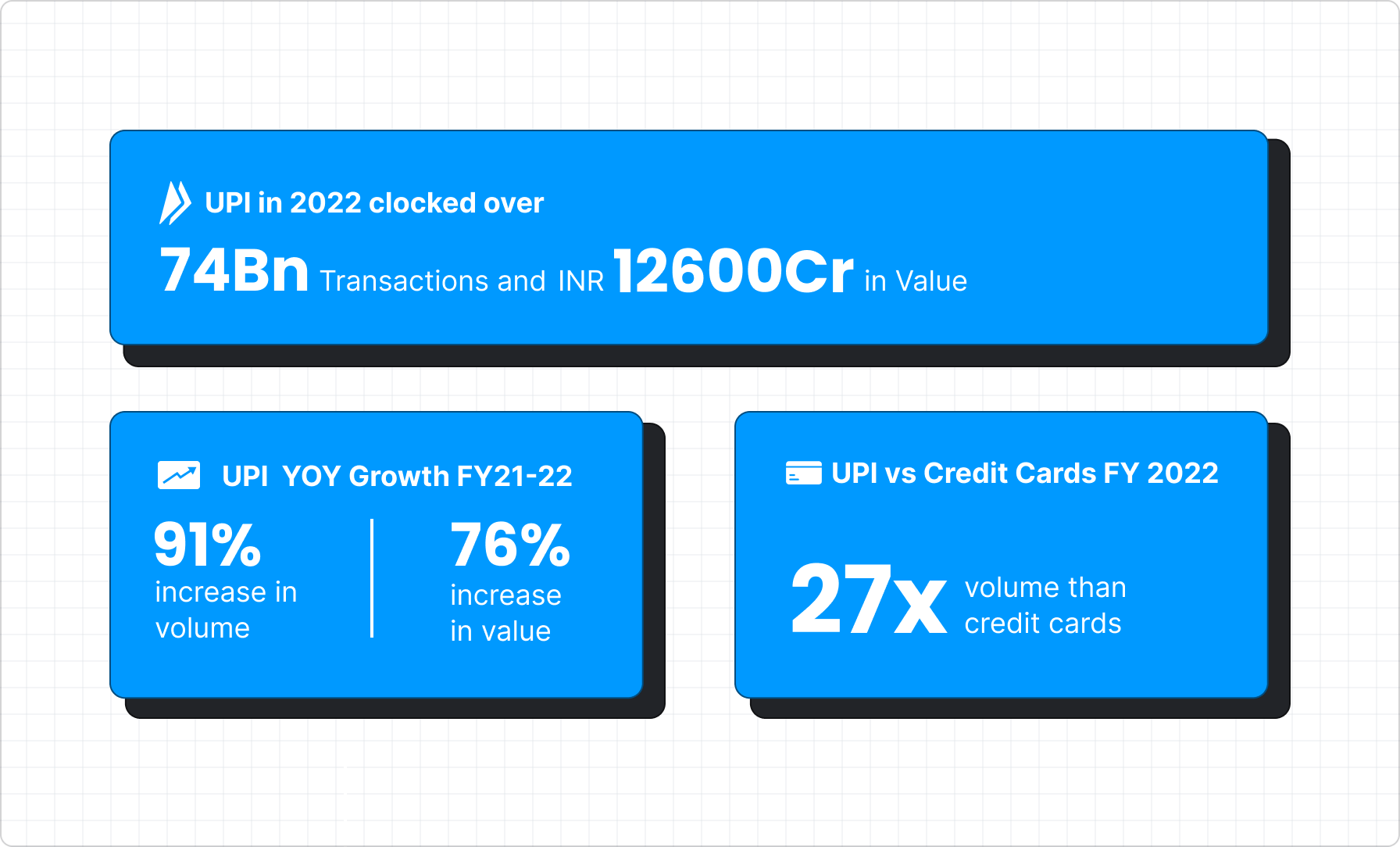

Payments in India mean UPI. It has become the most popular mode of digital payments in India. UPI in 2022 clocked over 74 Billion transactions and INR 12,600 Crore in value.

-

Almost Double than last year with a 91% increase in volume and over 76% increase in value.

-

Almost 27x the volume on Credit Cards and 10x the value.

UPI has changed the way people pay each other and merchants. In the early days, Peer to Peer (P2P) payments were predominant, but as with any Payments form factor, the actual multiplier effect unfolds when Peer to Merchant(P2M) starts growing.

The UPI Growth Story

BHIM - The Catalyst

It started with BHIM in 2016. And PSP apps such as Phonepe and Gpay ushered in the dominance that UPI enjoys today. However, merchant payment acceptance is more complex than P2P as the scale is less distributed, and the acquiring partner has to play a critical role in enabling merchants to accept payments seamlessly.

UPI Collect & UPI Intent - Accelerating Adoption

QR code has been a significant factor in increasing UPI’s offline acceptance. Still, online acceptance, especially in mobile apps, was initially dominated by UPI Collect, which was eventually eclipsed by UPI intent.

Today, UPI Intent is the dominant form factor in online UPI payments, especially on Android apps. (As per our data, 80% of merchant payments on apps are via UPI intent)

UPI Intent became popular as it is much simpler than UPI Collect, with almost no user data entry points. At Juspay, we still remember being the first to implement this for our merchants. Blinkit (ex-Grofers) was our first merchant, and today, top online merchants use the Juspay experience for powering intent journeys. Also, the scope of intent has increased from Android to iOS and even mobile web journeys.

In-App UPI Payments - A New Dawn

The Juspay UPI journey began in the days of BHIM and the UPI Common Library. And today, we power bank stacks for many TPAPs like Gpay, Amazon Pay, and Cred to big merchants like Swiggy, Bharatpe, Dream11, and BookMyShow.

We have always believed that UPI potential is much more. To further accelerate and widen the adoption, we need excellent infrastructure and even better customer experiences to make payments to merchants. And NPCI knows this better than anyone.

Last year, the umbrella organization created a circular to help merchants enable native UPI payments via the UPI plug-in SDK.

And today, we’re excited to announce the JUSPAY HyperUPI, in partnership with Yes Bank - the Plugin SDK for merchants to power in-app UPI Payments in their apps!

HyperUPI: In-App UPI Payments.

You must have seen this on CRED - paying your credit card bill is seamless without any switch to your UPI app for approving the Payment.

Don’t let the simplicity of this experience distract you from the fact that this implementation involves a lot of heavy lifting by the merchant. You essentially need to become a Third Party Application Provider (TPAP). This process entails messy regulations and costs, which are quite a task for merchants not aspiring to be Fintech/Payment companies.

So, we built it.

We built the in-app UPI experience for Cred and Amazon. And with the new NPCI guidelines, you too can now offer your customers an in-app UPI payment experience without needing to become a full-fledged UPI App.

HyperUPI Flow

Any merchant app can now become a UPI app and offer customers a completely In-app UPI payment experience.

Let’s examine how In-app UPI Payments differ from UPI Intent.

HyperUPI vs. UPI Intent

You’re ordering food on Swiggy. You find your favorite dish, add it to the cart, and proceed to checkout. You click on “Google Pay” (or any other UPI app option), are redirected to your Google Pay app, are asked to confirm the amount, enter your MPIN, and patiently wait for your food to arrive.

This UPI Payment flow is called UPI Intent.

Imagine no redirection to your Google Pay app in the above example. Your MPIN screen opens up directly in the Swiggy app, thereby simplifying the process with fewer clicks and hops - Seamless and in-app.

This UPI Payments flow is called In-App UPI.

What was a 6-step process with room for customer drop-offs is now essentially a seamless 2-step process in the merchant app itself.

HyperUPI Onboarding Flow

Let’s understand how customers can start using In-App UPI Payments.

HyperUPI Payment Flow

With Registration done, customers can now experience native and in-app UPI Payments.

Benefits of HyperUPI

In-App UPI Payments mean an Exceptional Customer Experience & Payment Conversions for merchants.

Better Customer Experience: Embedded or In-App UPI Payments lead to frictionless customer experiences. Embedded Payments also allow for better visibility over the entire customer purchase funnel.

Higher Conversions: No Additional hops to third-party UPI Apps mean merchants can now enable UPI for customers on their app and provide an unbroken experience. This Frictionless state leads to better conversions and, ultimately, better retention owing to a simple and seamless payments experience.

Lesser Drop Offs: A two-step process leaves less room for customers to drop-offs compared to the 6-step process in UPI Intent. Zero redirections to external apps reduce the scope of non-technical errors.

Higher Success Rates: 90% + Success Rates with lesser drop-offs and a seamless in-app process.

Better Customer Insights: In-App UPI Payments allow greater depth of visibility on the entire customer journey. You can understand why and where customers drop off and accordingly retarget them.

HyperUPI Use Cases

The embedded or in-app UPI payments flow ushers in a new era of simplicity and experience for Payments between customers and merchants. Some of the key use cases where HyperUPI can be a true differentiator include -

High-frequency purchases. Quick payment completion time and better conversions mean better loyalty and retention. Customers can directly see their masked bank account at the checkout and select which one to pay with. UPI lite can even make such payments essentially zero-click as customers won’t be required to enter a pin for transaction size <200.

Recurring Payments. UPI Autopay adoption is increasing and will be the mainstay for businesses collecting recurring payments. RBI guidelines on recurring payments have necessitated much more control to increase the success rate, e.g., Notification optimization and visibility into customer actions become very easy if a merchant uses Plug-in SDK for recurring payments.

Third-party verification. Many merchants, especially the mutual funds and securities segment, need control over bank account selection as the regulation only requires them to accept payments from a particular bank account. Currently, most such merchants depend on the Payment Aggregator/Bank partners for this. However, with merchant plug-in SDK, merchants have much more control over initiation and, thus, better conversions and lesser issues.

Omni Channel. Multiple merchants have both offline and online presence. At offline outlets, merchants can build end to end payment acceptance ecosystem such that QR codes can be by the merchant and even Scan n Pay functionality be provided in the merchant app for users.

In-App UPI Payments with Juspay HyperUPI

UPI Payments are having their “Amazon’s 1-Click button for ordering” Moment with the in-app payment flow. Since we wrote BHIM’s first line of code, our vision has always been to usher India into an age of frictionless payments. Our years of experience running UPI stacks for CRED & Amazon and building multiple SDKs for India’s startups are baked into this product.

Juspay & UPI - Building for India, building for you.

At heart, we’re still the young folks who built BHIM in 3 weeks, a campus for engineers, designers, hustlers, and storytellers who fall in love with the hard problems. We have grown a lot stronger, more reliable, and more robust since then.

Best-in-class UPI experience. We built and ran our own UPI switch, and there are no wrappers/third parties between us and NPCI.

*** A decade and Million SDKs later:** Juspay Safe SDK has optimized payment experiences for over ten years in Amazon, Flipkart, and Swiggy. We understand merchant payments, merchant pain points, and merchant asks. The Juspay blue loader is now ubiquitous across top apps and websites.

*** Building for you:** The Common Library in 2016, then BHIM, 99#, bank switches, and TPAPs. We love building for the nation and are grateful for the opportunity to contribute to the UPI revolution.

*** At the heart of UPI:* Being core contributors to UPI components has helped us translate those understandings into our product.

*** Collaborators:** UPI is a solution that involves working closely with banks, not just as a partner but as a contributor. Our relationship with banks is not just as acquiring partners; we are also TSPs who have built stuff for our banking partners. We are grateful to our banking partners for this trust in us.

Get on board.

Juspay is a part of the growth story of CRED, Dunzo, Swiggy, Zepto, and many more of India’s startups leveraging Payments to Grow and scale. HyperUPI In-App Payments elevate your Customer experience to levels that were inaccessible before, shrouded under complex compliance. With NPCI’s vision and our execution, in-app UPI Payments are now just a simple integration away.

Drop us a message here or at biz@juspay.in to elevate the UPI experience for your customers.